》Check SMM Lead Product Quotes, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

》Click to Access the SMM Database

SMM, January 8:

As mid-January 2025 approaches, how is the raw material stockpiling situation of secondary lead smelting enterprises? Is there resistance to the upward movement of battery scrap prices? This topic has drawn significant market attention.

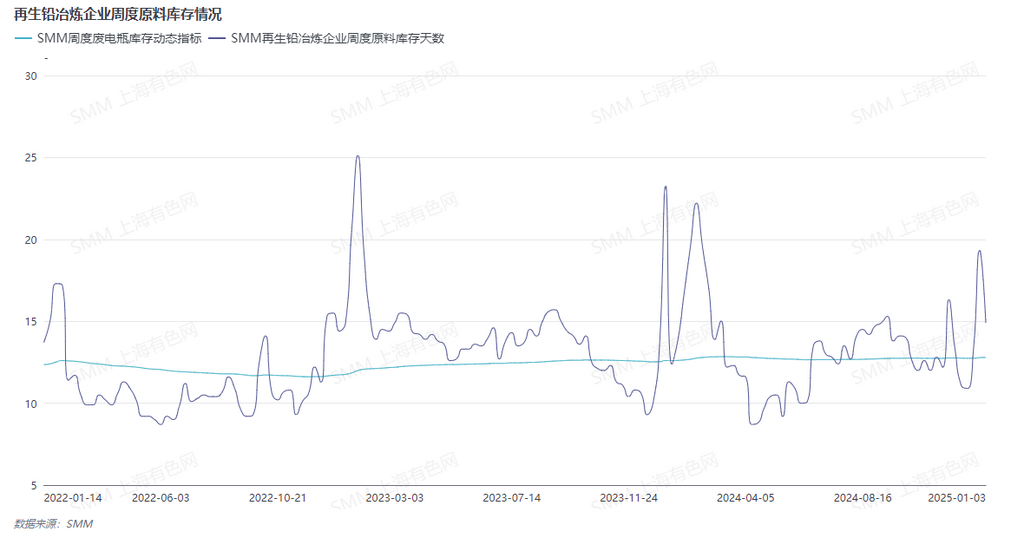

From the weekly raw material inventory perspective, as of January 8, data shows that the days of inventories for lead-containing scrap are approximately three days above the historical dynamic average, theoretically indicating a slightly loose raw material inventory situation for smelters.

Last week, due to environmental protection-related controls in Anhui, local smelters faced production constraints, leading to slow raw material inventory consumption. With production resuming this week, the raw material inventory level is expected to decline at a faster pace. Notably, this week saw new shutdowns for maintenance at medium and large secondary lead smelters, with these smelters stating that they would prepare to purchase raw materials only after confirming production dates post-holiday. This suggests that pre-holiday raw material purchasing demand has eased.

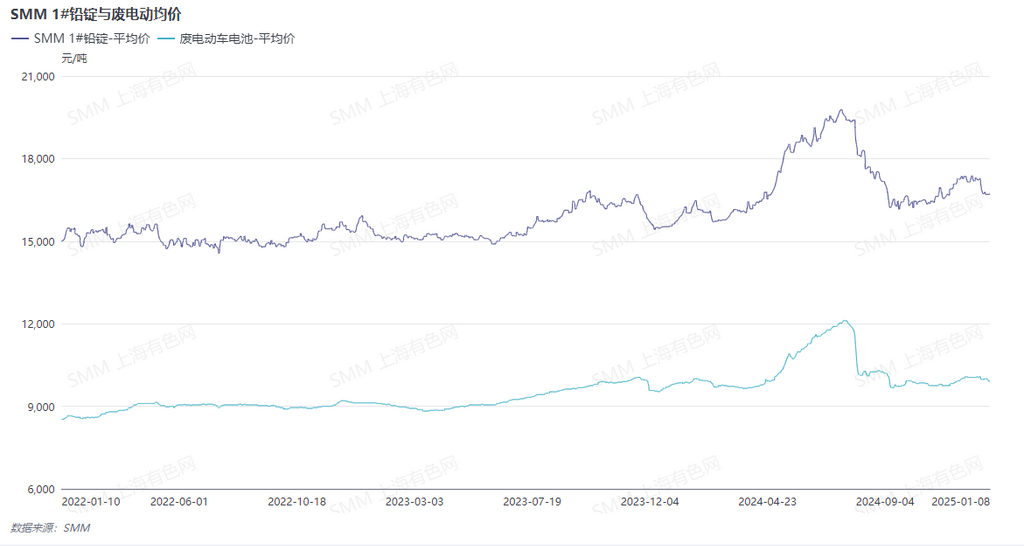

Currently, large secondary lead smelters in Jiangsu, Inner Mongolia, Shandong, Shanxi, and Anhui have all halted production. Before these shutdowns, most smelters had nearly depleted their raw material inventories. Some enterprises are still purchasing at low prices, while most indicate they will resume purchases after the holiday. Based on SMM's experience, with delayed post-holiday resumption by battery scrap recyclers and high procurement demand from smelters, battery scrap prices may see a significant increase after the holiday. Recently, due to insufficient stockpiling willingness from downstream battery producers ahead of the Chinese New Year holiday, lead prices have fluctuated rangebound with limited rebound potential. Under insufficient profit margins, the price increase for battery scrap purchased by secondary lead smelters has been slow.

In summary, pre-holiday raw material stockpiling demand from secondary lead smelters still exists, but the supply-demand imbalance is not prominent. Battery scrap prices have room for pre-holiday increases, though the rise is expected to be moderate. Attention should be paid to the impact of post-holiday resumption arrangements by secondary lead smelters on battery scrap prices.